US$ Euro Yen

North America

Caribbean

Central America

South America

Western Europe

Eastern Europe

Russia

Former USSR

Middle East

North Africa

West Africa

East Africa

Southern Africa

South Asia

Pacific Rim

Commodities

Multinational

December 3, 2019 (see December 18 update below). Next update: January 1, 2020. Visit Search to look at past issues of World Currency Observer (brochure edition).

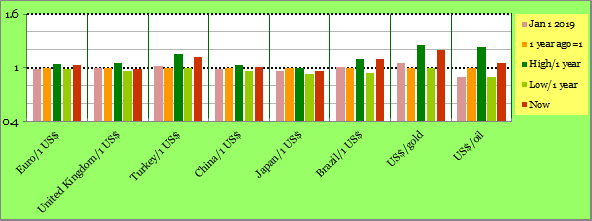

After weakening in October, the US dollar generally moved up against currencies around the world in November. The Iceland króna rose by nearly 1.5% against the US$ in November, and is now up by 2% since this time last year, The Mexico peso fell by 2.3% against the US$ in November. An increase of nearly 3.5% by the Costa Rica colón against the US$ left the colón up by 6,5% against the US$ since this time last year - the only other currency in the Caribbean/Central America which has risen since this time last year (although by much less) is the Trinidad and Tobago dollar. The Chile peso is down by more than 21% against the US$ since this time last year, after a 10% fall in November. The Brazil real fell by nearly 6 1/2% against the US$ in November (down nearly 10% since this time last year). The Euro fell by nearly 1.5% in November against the US$ (partly reversing an increase against the US$ in October), and the UK pound was up by nearly 1.5% against the Euro (down slightly against the US$). The Euro is down nearly 3% against the US$ since this time last year. The Hungary forint fell by 3% in November against the US$. The Poland zloty gave back part of the October 4.5% rise against the US$, falling by 2% in November - recent developments in the years-long ongoing court cases of private mortgages denominated in Swiss francs suggest that banks in Poland may have to accept repayments in Poland zlotys, with large losses involved. The Moldova leu rose by nearly 2% against the US$ in November - Moldova borders on Romania, whose currency is Euro-influenced, and on Ukraine. The Ukraine hryvnia rose by nearly 2% against the US$ in November, and is up by nearly 15% against the US$ since this time last year, while the Russia rouble is up 3 1/2% against the US$ since this time last year. The Israel shekel rose by more than 1.5% against the US$ in November, and is up by 6 1/2% against the US$ since this time last year. In Lebanon (and also in Syria, whose citizens have strong financial links to Lebanon), the usual gap between the official exchange rates (which have not moved much for some years for both countries) and the parallel exchange rates of each of the two countries, have widened considerably at the end of November, as the shortage of foreign exchange in Lebanon continues to be felt; private banks in both countries have sharply restricted withdrawals of US dollars and other hard currencies, but, despite these shortages, it is also reported that Lebanon was able to make a U$1.5 billion payment for a maturing bond issue. The Zambia kwacha fell by 10% against the US$ in November, and is down more than 20% since this time last year. The South Africa rand, in November, moved up by 2 1/2% against the US$. The Seychelles rupee and the Mauritius rupee each moved up by around 4% against the US$ in November, and the Madagascar franc was up by around 1 1/2%. The Australia dollar fell by over 2% against the US$ in November, leaving it down more than 8% against the US$ since this time last year. The New Zealand dollar moved down slightly in November, and is down just over 7% against the US$ since this time last year. The Myanmar kyat rose by 1.2% against the US$ in November, and is now up by 3.5% against the US$ since this time last year. The Thailand baht is up by more than 8% against the US$ since this time last year. Gold prices were down around 6.5% in November, due mostly to a fall to around US$1460/oz. early in the month. Oil prices moved down a little in November, but are still up around 6% since this time last year. Coffee prices are up around 13% on the month.

There were several media reports (Bloomberg and Middle Eastern media outlets) that, in a private talk to a legislative caucus of his party, the President of Turkey (Erdogan), urged citizens to convert their holdings of foreign currency (apparently mentioning both US dollars and Euros) into the Turkey currency (lira), something he has suggested before several times. It is very unusual these days to hear such an appeal by a major political figure (one reason: in many countries there is a legal requirement to make such conversions), although one should not underestimate the number of people in any country, including the United States, who think it is unpatriotic to hold too much foreign currency for too long without converting it into domestic currency (even if they are unaware they may hold such currencies indirectly through their investment holdings). One alternative for holders of hard currency: buy the sovereign debt of their country which is denominated in US dollars.

Those who follow foreign exchange issues are constantly reminded that cash is still widely used around the world, and that its conversion is still a major influence on foreign exchange rates, even though the mid-point rate for cash currency exchange (the benchmark that we rely on for analysis) is often buried deep within wide buy/sell quotations. Experienced travellers (like WCO staff) know that if you are travelling around in any country (outside the centers of major cities), that you should have cash (local currency) with you, lots of it, because that is still how businesses want to be paid, particularly for the things that tourists buy (meals, accommodation, taxis), even if they say they will “accept” credit and debit card payment – the use of cash is a preference, not always a necessity. There are lots of reasons for this, which vary from country to country. For transactions within countries for “non-tradeable” services and goods, even when the banking and credit card system is good or excellent (such as Switzerland and Germany), card transactions means additional costs for buyers and sellers – cash is preferred, if possible, please. And there are still plenty of countries where the cost to the average citizen to participate in the financial institutions sector is viewed as too expensive, so the cash economy is large (examples include Mexico and India). The use of cash would be even greater if it were less costly to make remittances by migrants to their home countries – small low-cost remittance businesses (many of which were very informal) were clobbered everywhere in the world after the World Trade Center bombing, on the grounds that they could be used to finance terrorism, which was surely a small part of their activities. One result is that remittance-based payments and transfers in many countries, such as in Africa countries (a huge source of foreign exchange for them), are made by cell phone credits, without cash and without the involvement of financial institutions. Of course, Cuba, a unique target of comprehensive United States sanctions, is almost 100 per cent cash-based. And, with regard to cash-based illegal transactions (drugs, tax evasion, criminal activities in general), the amounts involved are generally so large that the first task of any money launderer is to somehow convert the physical cash (large volumes of paper, vulnerable to theft, fire, water and every type of physical damage), as quickly as possible, into financial institution deposits, whose ownership can be firmly legally based and yet still disguised, and which can be transmitted around the world in seconds.

To round off the first week of December 2019: right now we are awaiting several events, including the United Kingdom election (Brexit, etc.), the results of China-US trade talks and what they will mean for tariffs scheduled to go into effect on December 15, and the next steps by the US Federal Reserve system with regard to interest rates. Also of importance, though perhaps of less risk, is progress on ratification by the US Congress of the update to the North American Free Trade Agreement, at the same time that Congress is looking at impeachment of the US president.

The events of mid-December flagged by World Currency Observer (see above) turned out largely as expected…The majority received in the United Kingdom elections by the Conservatives (Boris Johnson) is as strong a guarantee as could ever exist that the exit of the United Kingdom from the European Union will occur in January 2020 (i.e., there is no doubt now that Brexit will happen, but, unless there is a no-deal “hard” Brexit, there are many terms and conditions yet to be determined)…The United States and China reached agreements, so that the scheduled December 15 US tariffs did not happen, and some previous tariffs will be rescinded – perhaps other tariffs and restrictions will be unwound in the following months (the US noted there are still punitive tariffs on around $370 bn of China imports). One wrinkle is that that the refusal of the US to appoint members of the World Trade Organisation appellate panel means that the WTO dispute settlement process is “broken”, but this could be reversed quickly if the US chooses to get the process moving again (and, of course, the WTO rules that regulate world trading relationships are still in place)…The United States Federal Reserve has indicated no more downward movement in US interest rates for the moment (but, there is continuing news that the Federal Reserve has been intervening in the repo market to soften upward pressure on US interest rates)…The implications for foreign exchange markets of all these events will take some weeks to sort out, but there is a consensus that most-feared outcomes were avoided.

Some comments on conceptual and definitional issues. Two currencies can move together in the same direction if both offer products that are substitutes for each other, which therefore compete with each other. So, a rise in the value of one currency will result in foreign customers shifting their demand to products priced in another currency, which will put upward pressure on the other currency. (An example: upward pressure on the China yuan putting upward pressure on the Vietnam dong). And, what about two currencies which are linked together by a supply chain, with one country producing an intermediate product which is used in another country to manufacture a final product? Then it will depend upon which country produces the final product. An increase in the value of the final product country currency will reduce demand for the final product, which will reduce demand for the intermediate product country, and therefore put downward pressure on the intermediate product country currency. On the other hand, an increase in the intermediate product currency will raise the price of the final product good (to cover the increased costs), which will reduce demand for the final product, and therefore put downward pressure on the final product currency.

And a quick observation on CTA-motivated participation by commercial firms in currency futures markets, generally firms whose core business activities generate foreign exchange exposure. Under accounting rules, foreign currency assets and liabilities in the balance sheets (that is, foreign to the “functional currency” which each firm decides to use for its balance sheet, usually the one in the country where it has its greatest business activity) are adjusted to the market value of exchange rates every year, creating the possibility of foreign exchange gains or losses each reporting year (often recorded in financial statements by use of the term “cumulative translation adjustment”, CTA for short). The necessity of reporting this paper gain or loss gives rise to what may be termed as “defensive participation” in currency futures markets, by companies who at least want to avoid any currency movement financial losses from their assets and liabilities, which would undermine the profits and losses from their core business pursuits. Of course, this is not the only motivation for commercial firms to participate in currency futures markets – there will be day-to-day business transaction exposure related to hedging and funding future cash payments and receipts in foreign currencies. But recognition of asset-related CTA activity by commercial firms is often remarked upon by analysts, who like to differentiate long and short positions taken by different groups of market participants (such as dealers (brokers), asset managers (pension funds, life insurers), leveraged firms (hedge funds)) for indications of market views on the future movement of currencies.

(World Currency Observer will next be updated on January 1, 2020. Visit Search to look at past issues of World Currency Observer (brochure edition). For permission-to-quote enquiries, e-mail World Currency Observer at WCO@briargreen.com.)