US$ Euro Yen

North America

Caribbean

Central America

South America

Western Europe

Eastern Europe

Russia

Former USSR

Middle East

North Africa

West Africa

East Africa

Southern Africa

South Asia

Pacific Rim

Commodities

Multinational

August 2, 2017 (see August 16 and August 30 updates below). Next update: September 6, 2017. Visit Search to look at past issues of World Currency Observer (brochure edition).

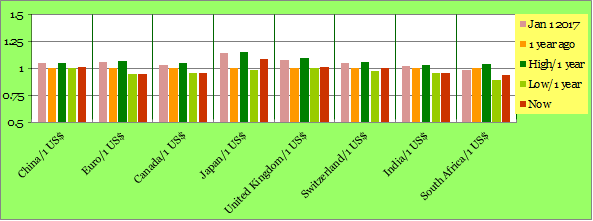

A quick test of the widespread observation of weakness of the United States dollar against a broad range of currencies suggests that this story is a better fit for comparisons with start-of-2017 exchange rates rather than one-year-ago exchange rates–for instance, see the currencies in the above chart. Using the Japan yen as an example: while it has strengthened by 1.5% against the US dollar in July, and has risen against the US dollar since the beginning of 2017, nonetheless, the yen is down nearly 8.5% since this time last year. Looking at the Euro as another example: the Euro was up nearly 3% in July against the US$, and up by 5% since this time last year, but it is up even more strongly compared with its US dollar value at the beginning of the year.

Looking at exchange rate developments in the other countries of the world, starting with countries bordering the United States: the Canada dollar was up over 4% against the US$ in July, and is now up nearly 5% since this time last year and the Mexico peso is up 5.5% since this time last year. The Iceland króna is up nearly 14% against the US$ since this time last year. The Costa Rica colón is down 4.5% against the US dollar since this time last year, and the Nicaragua córdoba is down over 5%. The Argentina peso was down nearly 9% against the US$ in July, but all other South America currencies were up, with the Brazil peso up by a strong 5% on the month against the US dollar. The Swiss franc fell by 1% against the US in July, and is at roughly the same level as this time last year. The Turkey lira fell by a little against the US$ in July, and is down 17% since this time last year. Other currencies in Eastern Europe were generally stronger in July against the US$ than was the Euro - the Czech Republic koruna is up over 9% since this time last year. The Russia rouble is more than 10% stronger against the US dollar than this time last year, and the Ukraine hryvnia is up by around 4.5% since then. The Iran rial fell by nearly 3% in July against the US$, and is down 21% since this time last year. African currencies were generally up against the US dollar in July, with the exceptions of Democratic Republic of Congo (down 7.4%), and the Sudan pound, which fell by 9% on the month. Asian currencies were generally stronger against the US dollar in July-one exception was the Mongolia tögrög, down nearly 4% on the month, and down 18% against the US$ since this time last year. Oil prices in US dollars were up more than 7% in July, and have risen by 20% since this time last year (and are down 7.5% since the beginning of 2017).

Among the many news items in July on US sanctions against foreign countries and nationals were: the US Congress moved to embed many of the sanctions against Iran, North Korea and Russia in legislation, which would make them harder to remove in future (like for Cuba); talk of US sanctions against imports of oil from Venezuela; a delay in removal of sanctions against Sudan; and a threat by the European Union to retaliate against the US if planned sanctions related to Russian gas exports harm European firms. The list of countries against whom the US maintains sanctions includes: Burundi, Belarus, Central African Republic, Cuba, Iran, Libya, North Korea, Somalia, Sudan, Syria, Russia (related to Ukraine, and also to former hedge fund manager Sergei Magnitsky), Yemen and Zimbabwe. There are additional sanctions which are applicable to persons undertaking undesireable actitivities in a list of countries, which include: the Balkan countries, Democratic Republic of the Congo, Iraq, Lebanon, South Sudan and Ukraine (Russia-related). There are also multi-national sanctions related to activities by transnational criminal organisations, violations of nuclear non-proliferation, trade in conflict diamonds, narcotics, terrorism and cyber crimes.

CarSpring International has published data on the prices of standard taxi rides in 80 locations (around 60 countries) around the world, converted to US$, Euros, and United Kingdom pounds at beginning-of-June-2017 exchange rates. The Economist magazine publishes similar data on the price of McDonalds restaurant Big Mac hamburgers in a large number of countries every three months, which it then converts to US dollars at the current exchange rate. The Economist goes one step further, by comparing the US dollar price of the Big Mac in each country with its price in the United States – in theory, a too-high-price in a foreign country means an overvalued currency, and a too-low-price means undervaluation. The same exercise can be performed with the taxi-ride data for the three currencies. WCO remarks that, to us, the most interesting observations include: the wide dispersion of prices in Europe, far exceeding the in-USA dispersion (strikingly, not that much variation between Los Angeles/San Francisco and far-way New York City), and that the taxi data implies, using the Economist technique, that the Swiss franc and Japan yen are strongly overvalued.

With regard to over-valued and under-valued currencies: the recently-released IMF External Sector Review compares the inflation adjusted exchange rate (the real exchange rate) for 20 countries with their current account deficits, to come up with a measurement indicating over or undervaluation of the currency. One feature of the IMF approach is the recognition that, in some cases, action by one country can change the current account in another country, to such an extent that less action (such as a change in the exchange rate) may be recommended for the second country to remove its own imbalance. The IMF paper says that its analysis suggests the US dollar is overvalued by 5 to 15%, and that, in the case of Germany, the Euro is undervalued by the same amount. For some other Euro countries, the Euro is viewed as overvalued, in which case it is recommended that they take “steps” to boost their external competitiveness –in the case of German overvaluation, spending increases are recommended. Other countries deemed as having undervalued exchange rates (outside any gap range) include: Mexico, Malaysia, Netherlands, Singapore, South Korea and Sweden.

The Malaysian central bank (Bank Negara Malaysia), to discourage internationalisation of the Malaysian ringgit, has reminded financial institutions not to engage in offshore trading of the ringgit, which includes not participating in trade in the ringgit futures contracts recently introduced on the Singapore Exchange and the Intercontinental Exchange (ICE). Foreign entities were also reminded to obtain their ringgits in the Malaysia onshore financial markets.

Recent additional sanctions on North Korea include coal, iron and iron ore, lead and seafood, intended to cut North Korea exports, currently estimated at US$3 billion per year, by a third. Many of these exports go to China. North Korea is unique in the world of currencies, as a country with an official legal exchange rate and a highly illegal parallel rate. (In other countries, at the current time, parallel markets for foreign exchange have generally evolved as a consequence of governments trying to manage shortages of foreign exchange. WCO rejects as simplistic the idea that all parallel currency situations can be lumped together under the “troubled currency” heading.) The North Korea official rate is 108 won/1US$, and the number of sources giving indications of the official value of the won dried up around 2 years ago, as sanctions against trade with North Korea began to bite, reducing the need for won quotations. There are indications that quotes of the parallel value of North Korea won have been in the 8000-8100/1$US range for much of 2017 (touching the 8100 level recently) and that, so far, the won is actually stronger in 2017 than it was last year.

Reflecting on the currency episode which took place in the market for the Pakistan rupee at the beginning of July (see WCO July 2017), debate about the appropriate level of the rupee has long been at the heart of economic discussions in Pakistan. Political support for a strong rupee (as a by-product of policies aimed at import substitution and development of in-Pakistan goods and services production) has long been at odds with a view that the rupee has been overvalued for more than 10 years, reducing international competitiveness of Pakistan exports - the latest thinking (fed by a December 2016 remark by an IMF official) is that the rupee is overvalued by 5 to 15% against the US$. It is remarked that the current account effects of the too-strong rupee, on imports and exports of Pakistan tradeable goods, are offset by remittances from abroad of Pakistan expatriates living and working in other countries (comparing their current account impact with other countries, they are among the highest in the world), by loans made to Pakistan by multilateral institutions (Pakistan has long been an IMF client), and, now, from current and future investments from China under the One Road One Belt program, which has specifically targeted Pakistan to be a major recipient of funds.

And, to touch on another item from the July 2017 WCO, the value of the bitcoin has rebounded sharply in the last month-and-a-half, obliterating the earlier decline, and has recently reached new highs of nearly US$4400/bitcoin, well above the former peak of US$3000/bitcoin (currently trading at around US$4200).

A possible trade war in the Balkan region of Eastern Europe, which could have been very ugly, was avoided in August, between European Union member Croatia, and non-EU members Bosnia-Herzegovina, Macedonia, Montenegro, and Serbia, when Croatia dropped plans to continue with a previously announced increase of import fees for fruits and vegetables (related to Europe-mandated pest and virus inspection), going into effect right in the middle of the summer harvest-time. While the fees were imposed by Croatia to comply with what it saw as EU requirements, and applied to all non-EU members, the four Balkan states in question would be the hardest hit (also hard-hit would have been Kosovo). Making this more complicated is that Russia has, in retaliation against EU sanctions, imposed an embargo on the import of fruits and vegetables from the EU, so the Croatia move might have played some part in this. The EU response to Russia has included the announcement of support measures for EU growers, including Croatia, which was a strong incentive for Croatia to comply with the inspection rules. Also complicating the case from Croatia’s standpoint is that it is currently dealing with the almost-bankruptcy of Agrokor, a major Croatian food company (production, distribution, transportation and retail of food products) with operations throughout the Balkans, which got into financial problems due to too-rapid expansion. The four Balkan countries are the current core members of the Central European Free Trade Agreement, to which Croatia used to belong until it joined the European Union. The US$ value of the currencies of all the countries involved in this dispute are either pegged to, or heavily influenced, by the Euro. Croatia has been working hard to reduce its fiscal deficit and debt, in order to join the European Union Exchange Rate Mechanism II (+/-15% band around a central exchange rate), as a step towards eventually adopting the Euro.

(World Currency Observer will next be updated on September 6, 2017. Visit Search to look at past issues of World Currency Observer (brochure edition).)